Some Financial Thoughts for 2024

The time has come again to make some forecasts and predictions for the new year. But first, we take a look back at last year’s predictions and see how well we scored...

2023 Rewind

- 2023 Real GDP will be below 1%: No

- CPI will finish the year below 3%: No but close...

- The Fed will not hike rates above 5.25%: No but close...

- 10 year Treasury yield will not move above 4.5%: No

- The S&P 500 will retest its low but manage to finish the year higher: No/Yes

- High Yield credit will generate above 8% return: Yes

- The USD has peaked: Yes

- Oil will finish the year below $80: Yes

So 3 good calls, 3 kind of ok and 2 really off. Lots of lessons to be learned. Overall my assessment about the inflationary picture was relatively correct but my expectation on economic growth was off given the economy remained resilient.

Let's now look at how next year might look like, the overall theme could be described as “after the Fed is done hiking rates”.

2024 Forecast

- For the year the U.S. GDP will be above 2%

Calls for a recession might be premature. Helped with an ample budget deficit the economy will remain resilient in 2024. This is especially true as if the economy were to soften, the Fed has plenty of room to cut rates. The recent decline in both long term interest rates and oil price will also act as tailwinds for H1 growth.

- The U.S. budget deficit will remain larger than $1.5Tr

Last year the budget deficit was close to a staggering $1.7Tr. With no real push in Washington to have some fiscal discipline we expect next year's deficit to remain large, especially as we go through an election year. Welcome to the world of permanently large budget deficits (fueling inflation).

- Oil price will drop below $60

On the supply side, U.S. oil production is now making a new all time high (there is also supply growth in marginal producers such as Iran and Guyana). To combat this increase in supply, Opec has been reducing its production but without the expected result on prices. On the demand side world GDP will remain relatively muted given the low growth in Europe, China and U.S.. The net effect of ample supply with relatively weak demand would point toward lower prices, especially if Saudi Arabia decides to “flush the markets” with some increase in production.

- Core CPI will stay above 2%

While Headline CPI is likely to keep moving lower and be below 2%, Core CPI will remain firm due to the continued pent up demand in services and housing prices (helped by the recent decline in long term rates).

- High Yield Credit will generate more than 7%

In an environment with GDP growth above 2% and with the Fed being done with its interest rate hike, High Yield credit will perform well and generate more than 7% return in 2024.

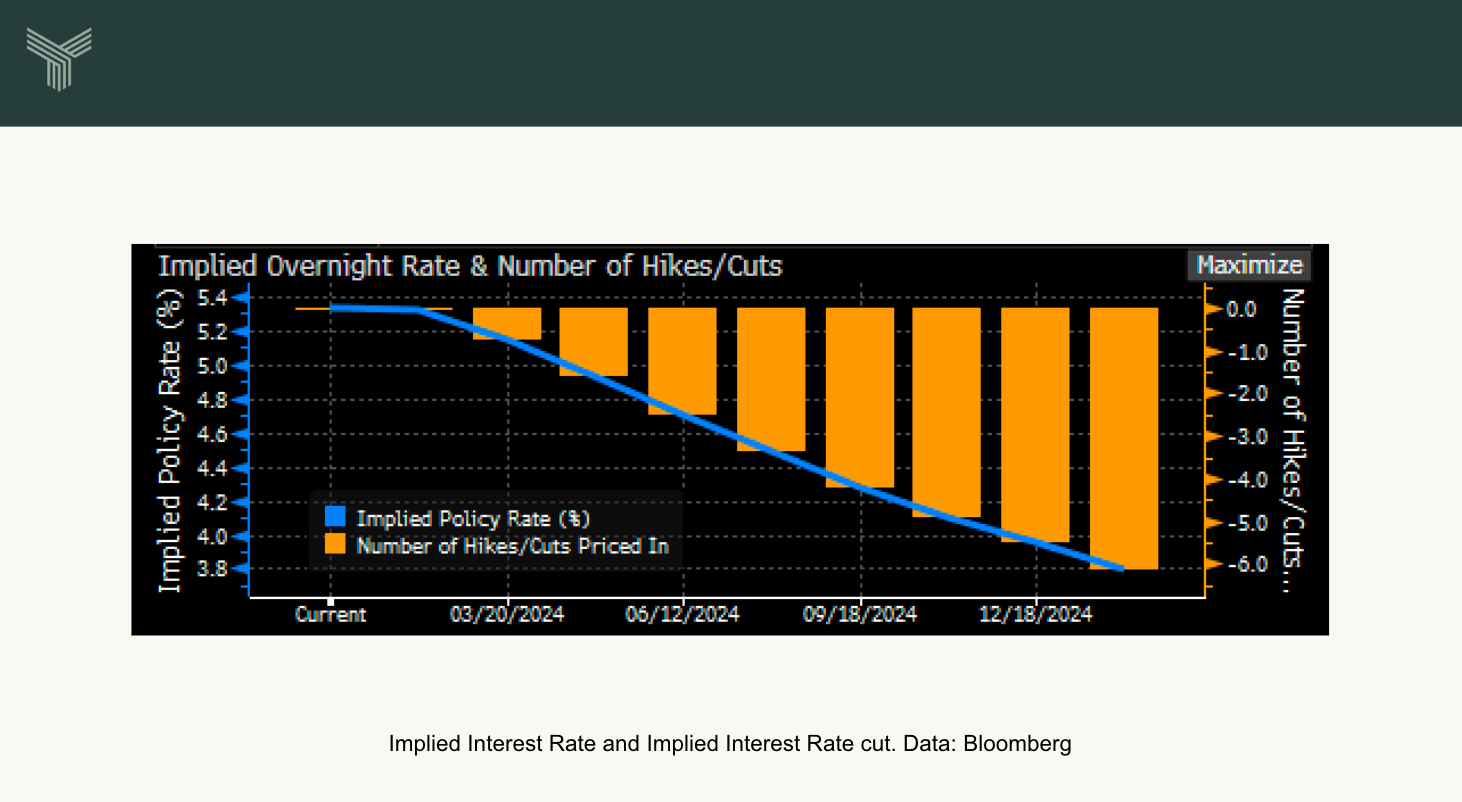

- Fed will not cut interest rates by 125bps

The markets are now expecting close to 125bps of interest rate cut next year. But with Core Inflation remaining sticky and above 2% and growth remaining reasonable with the Unemployment rate close to an all time low; the Fed will be in no rush to deeply cut interestrates.

- The 2 year Treasury yield will stay in the 4-5% range

Echoing the Fed standstill default stance, it is expected the 2 year Treasury yield will remain stable in the 4% to 5% range.

- The Risk Parity Portfolio will generate above 7.5% returns

The Risk Parity portfolio also known as the 60/40 Portfolio (ie 60% allocated to equities and 40% long term U.S goverment bonds) had some pretty bad performance in 2022 and most of 2023. For 2024 we expected an above average performance for the 60/40 Portfolio thanks to the Fed being done with its interest rate hikes.

Ben Verschuere

Chief Investment Officer

Disclaimer: Not investment advice. The views and opinions in this piece are just the author's own, offered to the public at large and not to any one particular investor.

.png)